Economies

Econometric Approaches: How Economists Turn Data Into Answers

Economics is full of questions that sound simple but are surprisingly hard to answer rigorously.

Does raising the minimum wage reduce employment? Does foreign direct investment accelerate growth? Do higher interest rates actually slow inflation, or does the relationship run the other way? Does education cause higher earnings, or do people who would have earned more anyway tend to get more education?

Everyone has an opinion. Econometrics is the discipline that tries to replace opinion with evidence — and to be honest about how strong or weak that evidence actually is.

What Econometrics Is Trying to Do

At its core, econometrics applies statistical methods to economic data to do three things: describe relationships, test theories, and make forecasts.

The challenge is that economic data is not generated by controlled experiments. In a laboratory, you can change one variable while holding everything else constant. In an economy, everything moves at once. Interest rates change when inflation changes when growth changes when expectations change. Isolating the effect of any single variable on another is genuinely difficult and the history of econometrics is largely a history of developing smarter ways to do it.

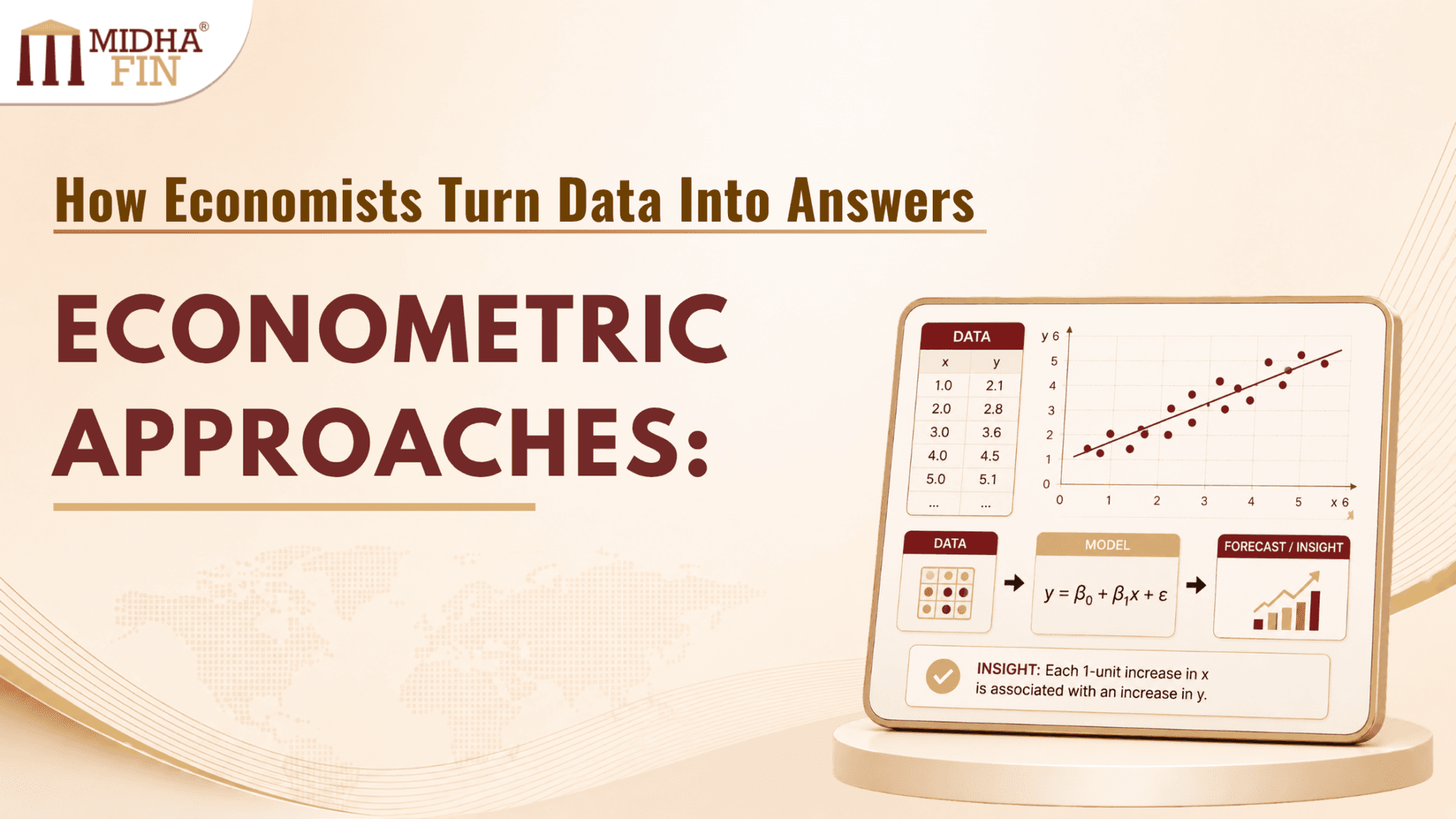

1. Ordinary Least Squares — Where Everything Starts

The simplest and most widely used econometric tool is OLS regression. It estimates the linear relationship between a dependent variable and one or more explanatory variables by finding the line that minimises the sum of squared differences between actual and predicted values.

In an economic context, a basic OLS model might look like:

Consumption = β₀ + β₁(Income) + β₂(Interest Rate) + ε

β₁ would tell you how much consumption changes for every one-unit increase in income, holding interest rates constant. This is the estimated marginal propensity to consume — a central concept in macroeconomics.

OLS works well when its assumptions are satisfied: the relationship is linear, errors are randomly distributed with constant variance, observations are independent, and explanatory variables aren’t too correlated with each other.

The problem is that economic data rarely cooperates on all these fronts simultaneously. GDP and investment move together. Inflation and interest rates are set in response to each other. Employment and wages are jointly determined. Every one of these situations creates estimation problems that a naive OLS application will get wrong.

2. The Endogeneity Problem Economics’ Central Headache

If there is one issue that defines econometric practice in economics more than any other, it is endogeneity.

Endogeneity occurs when an explanatory variable is correlated with the error term meaning it’s not truly independent of what you’re trying to explain. This breaks OLS. The estimates become biased and inconsistent, and no amount of additional data fixes the problem.

The classic economic example is the supply and demand system. You observe market prices and quantities. You want to estimate the demand curve how quantity demanded responds to price. But price and quantity are jointly determined by both supply and demand. You can’t simply regress quantity on price and call it the demand curve, because the price you observe is already shaped by both curves simultaneously.

The same problem appears throughout applied economics. Does more policing reduce crime, or do high-crime areas get more police? Does financial development cause economic growth, or does growth create demand for financial services? Does trade openness increase income, or do richer countries tend to trade more?

In each case, causality runs in multiple directions, and standard regression cannot untangle them.

3. Instrumental Variables Finding an Exogenous Lever

The instrumental variables approach is the primary solution to endogeneity in economics. The idea is to find an instrument with a variable that affects the endogenous explanatory variable but has no direct effect on the outcome except through that channel.

The instrument provides an exogenous source of variation in the endogenous variable. By isolating only the variation in the explanatory variable that is driven by the instrument variation that is clean of the endogeneity IV estimation recovers an unbiased estimate of the causal effect.

The two-stage least squares (2SLS) procedure implements this: in the first stage, regress the endogenous variable on the instrument and other controls. In the second stage, use the predicted values from stage one which contain only the exogenous variation in the main equation.

A famous example in development economics: researchers wanted to estimate the effect of colonial institutions on long-run economic development. But colonial institutions and development are jointly determined richer places may have attracted better institutions. The instrument used was settler mortality in colonial times. Places where European settlers faced high mortality from disease (like malaria-prone coastal regions) tended to develop extractive institutions rather than settler institutions. Settler mortality affected institutions, and affected development only through institutions making it a plausible instrument.

Finding instruments this creative and this defensible is genuinely hard. A weak instrument one only loosely correlated with the endogenous variable produces estimates that can be worse than OLS. The strength of an instrument is tested statistically (the F-statistic from the first stage should typically exceed 10), and its exogeneity, while not directly testable, must be argued on economic grounds.

4. Time Series Econometrics — Modelling Economies That Evolve

Much of macroeconomic data is time series GDP, inflation, unemployment, exchange rates, money supply recorded sequentially over time. Time series econometrics is built around the specific challenges this structure creates.

Stationarity

The first and most fundamental issue is stationarity. A stationary series has a constant mean, constant variance, and autocorrelations that don’t depend on time. Most macroeconomic series are not stationary GDP grows over time, price levels trend upward, populations expand.

Running regressions on non-stationary series without addressing the issue produces spurious regression relationships that appear statistically significant but are entirely meaningless. Two independent random walks will show high correlation simply because both trend over time. This is one of the most common mistakes in applied economic analysis.

Testing for a unit root the standard indicator of non-stationarity is therefore a prerequisite for time series work. The Augmented Dickey-Fuller (ADF) test and the Phillips-Perron test are the workhorses here.

Vector Autoregression (VAR)

When you have multiple economic variables that influence each other, say, GDP growth, inflation, and the policy interest rate a VAR model treats each variable as a function of its own lags and the lags of all other variables in the system.

VAR models are extensively used in macroeconomics for two purposes. First, impulse response functions trace how a shock to one variable, say, an unexpected interest rate hike propagates through the system over time, affecting GDP, inflation, and other variables across subsequent periods. Second, forecast error variance decomposition shows how much of the variability in each variable is explained by shocks to itself versus shocks to other variables in the system.

VAR was popularised partly as a response to the identification problems in large structural macroeconomic models. Rather than imposing a specific theoretical structure, VAR lets the data speak though the tradeoff is that interpreting the results requires additional identifying assumptions.

Cointegration and Error Correction

Sometimes two or more non-stationary series share a long-run equilibrium relationship; they may drift individually, but they don’t drift apart from each other indefinitely. This property is called cointegration.

The canonical economic example is the relationship between consumption and income. Both grow over time, both are non-stationary. But their ratio (the average propensity to consume) tends to be relatively stable over the long run. Consumption and income are cointegrated.

When cointegration is present, an error correction model captures both the long-run relationship and the short-run dynamics of adjustment back toward equilibrium when the series temporarily deviates. The error correction term is the key: it tells you how quickly the system corrects after a deviation from the long-run relationship.

Cointegration testing, particularly the Johansen test for systems with multiple potentially cointegrated series is standard practice in macroeconomic and international economics research.

5. Panel Data — Combining Countries, Regions, or Firms Over Time

Development economics, international economics, and labour economics all routinely work with panel data observations on multiple units (countries, states, households, firms) across multiple time periods.

Panel data is powerful because it allows economists to control for unobserved heterogeneity stable differences between units that might confound cross-sectional comparisons.

For example: if you want to estimate the effect of trade openness on economic growth using cross-country data, you face an immediate problem. Countries differ in culture, geography, institutions, and history in ways that affect both their openness and their growth, but that you can’t easily measure. A cross-sectional regression will attribute some of these unobserved differences to trade openness, biasing the estimate.

With panel data and fixed effects, you can control for all time-invariant country characteristics observed or not by essentially comparing each country to itself over time. The identifying variation comes from changes within countries, not differences between them.

Random effects models are more efficient when entity-specific effects are uncorrelated with the regressors, a testable assumption via the Hausman test. The choice between fixed and random effects is one of the first decisions in any panel data analysis.

More recently, two-way fixed effects controlling for both entity fixed effects and time fixed effects has become standard. Time-fixed effects absorb common shocks that affect all countries in a given year: global recessions, commodity price collapses, financial crises preventing these from contaminating the estimated relationship of interest.

6. Natural Experiments and Causal Inference

The most significant methodological shift in economics over the past three decades has been the turn toward causal inference explicitly designing the analysis around identifying causal effects rather than correlations.

This shift, associated with what some call the “credibility revolution,” recognised that observational data rarely allows causal interpretation without careful design. The solution was to find or construct situations that approximate random assignment natural experiments.

Difference-in-Differences

DiD is the most widely used natural experiment approach. It compares the change in outcomes for a group affected by some policy or event to the change for an unaffected group over the same period.

The intuition: if both groups were trending similarly before the intervention (the parallel trends assumption), any divergence after the intervention can be attributed to the intervention itself.

A classic application: Card and Krueger’s study of the New Jersey minimum wage increase in the early 1990s. They compared employment in fast food restaurants in New Jersey (treated) to those in Pennsylvania (control) before and after the wage increase. Contrary to the standard prediction, they found no negative employment effect, a result that sparked enormous debate and reshaped how economists think about labour markets.

DiD has grown considerably more sophisticated. Staggered DiD where different units are treated at different times is now common in policy evaluation, though recent econometric work has shown that naive staggered DiD estimates can be badly biased when treatment effects vary across units or time.

Regression Discontinuity Design

RDD exploits sharp cutoffs in assignment rules. If a government program is available to households below a certain income threshold, comparing households just above and just below the threshold who are otherwise very similar isolates the causal effect of the program.

The identifying assumption is that nothing else changes discontinuously at the threshold. Units just below the cutoff serve as the counterfactual for units just above (or vice versa). The local nature of the comparison makes RDD highly credible but limits generalisability; the estimated effect applies specifically to units near the threshold, not necessarily to the broader population.

Synthetic Control

When the treated unit is a single country, region, or city and finding a good control group is difficult the synthetic control method constructs a weighted combination of untreated units that closely matches the treated unit’s pre-intervention characteristics and trends.

The synthetic control then serves as the counterfactual: what would have happened in the absence of the intervention? Deviations between the actual outcome and the synthetic control after the intervention are attributed to the policy.

This method has been used to evaluate the economic effects of German reunification, the impact of terrorist conflicts on regional economies, and the consequences of specific trade agreements.

7. Structural Econometrics — Bringing Theory Back In

The credibility revolution, for all its contributions, has a limitation: reduced-form estimates answer “what happened” but often struggle to answer “why” or “what would happen under a different policy.”

Structural econometrics takes a different approach. It explicitly models the economic behaviour, the utility functions, production functions, market equilibrium conditions and estimates the structural parameters that govern that behaviour. Once estimated, the model can be used for counterfactual policy analysis: what would happen if the tax rate changed, if a new competitor entered, if a regulation were removed?

Structural models are computationally intensive and require strong theoretical assumptions. But they offer something reduced-form methods cannot: the ability to simulate policy scenarios that have never been observed in the data.

Industrial organisation the study of how markets and firms behave relies heavily on structural econometrics. Estimating demand systems, modelling firm pricing behaviour, evaluating merger effects all of these require structural approaches.

8. Forecasting Models — When Prediction Is the Goal

Not all econometric work is about identifying causal effects. Sometimes the goal is simply to predict what GDP growth will be next quarter, where the exchange rate will be in six months, and how unemployment will evolve over the next year.

Forecasting models are evaluated differently from causal models. A variable that has no causal relationship to the outcome might still be a useful predictor if it happens to correlate with it in a stable way. The metric is forecast accuracy mean squared error, absolute error, directional accuracy not coefficient interpretability.

ARIMA models, VARs, and more recently machine learning methods are all used for macroeconomic forecasting. The dynamic factor model which extracts common factors from a large number of macroeconomic series has become standard at central banks and forecasting institutions.

The empirical finding that simple time series models often outperform large structural models in out-of-sample forecasting was one of the early motivations for the VAR approach and remains a humbling result for macroeconomic modelling.

Choosing the Right Approach

| Economic Question | Appropriate Approach |

| Estimating relationships in cross-sectional data | OLS regression |

| Endogenous explanatory variable | Instrumental variables / 2SLS |

| Multiple jointly determined macro variables | VAR |

| Non-stationary series with long-run relationship | Cointegration, Error Correction Model |

| Policy evaluation with treated and control groups | Difference-in-Differences |

| Sharp eligibility cutoffs | Regression Discontinuity |

| Single treated unit, no natural control | Synthetic Control |

| Multiple countries or firms over time | Panel Data (Fixed / Random Effects) |

| Policy simulation and counterfactuals | Structural Econometrics |

| Pure forecasting | ARIMA, VAR, Dynamic Factor Models |

The Honest Disclaimer That Runs Through All of It

Every econometric approach rests on assumptions. Instruments must be exogenous. Parallel trends must hold for DiD. The cutoff must be sharp and not manipulated for RDD. Stationarity must be established before time series modelling. Fixed effects only control for time-invariant heterogeneity.

When assumptions are credible, the results are credible. When they’re not, when the instrument is weak, when treated and control groups were trending differently before the policy, when the series is non-stationary and the researcher didn’t check the estimates can be misleading in ways that aren’t always obvious from the output.

This is why reading econometric research critically means asking not just “what did they find” but “what did they have to assume to find it, and how plausible are those assumptions.” That question is at the heart of what it means to think carefully about economic evidence.