Equity

Preemptive Rights: Meaning, Example, and How It Works

Imagine baking a beautiful, eight-slice pizza with a group of friends. You paid for your share, so two of those delicious slices belong to you—exactly 25% of the pie. But just as you sit down to eat, the host invites four more people into the room and cuts the exact same pizza into twelve slices instead. Without taking a single bite or giving away your food, your share suddenly shrinks to less than 17%.

In the corporate world, this exact phenomenon happens to shareholders all the time. It is called equity dilution. To protect investors from having their “piece of the pie” quietly shrunk without their consent, corporate finance relies on a fundamental shield: preemptive rights.

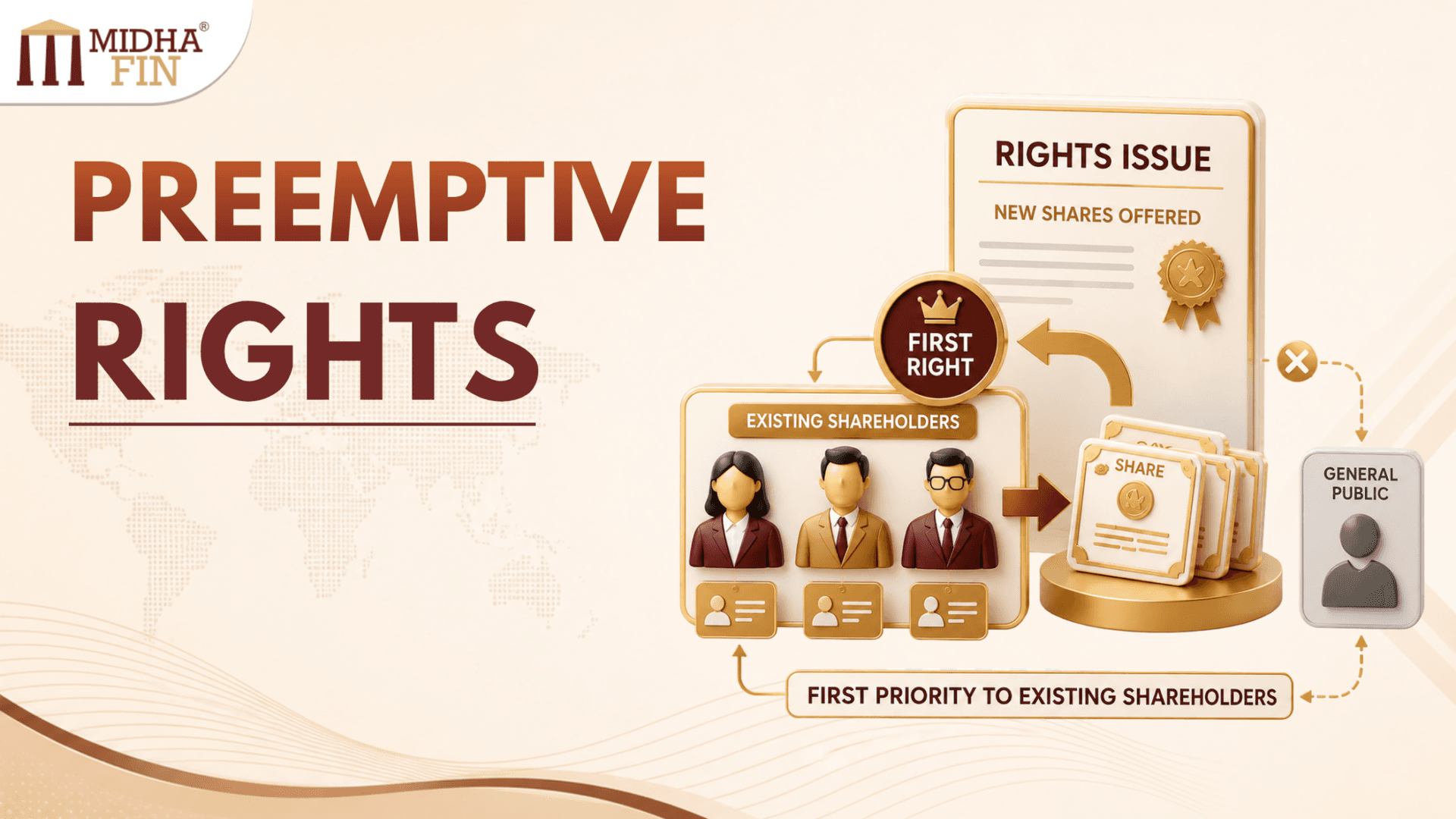

Preemptive rights give existing shareholders the legal right to maintain their ownership percentage in a company before any brand-new shares are offered to outside investors.

In simple terms, if a company decides to pull the trigger on a new share issuance to raise capital, you—as an existing owner—get the first opportunity to buy those new shares in exact proportion to what you already own. This right is also known as the “right of first refusal on new shares,” or more commonly across global financial markets, a rights issue entitlement.

What is Dilution and Why Does it Matter?

Before we dive into the mechanics of preemptive rights, we need to understand the financial problem they are designed to solve.

Let’s look at a quick math example: Suppose a company has 100 total shares outstanding, and you happen to own 10 of them. Your stake in the business is straightforward:

Ownership = 10 / 100 = 10%

Now, suppose management decides to issue 50 entirely new shares to raise fresh capital for a new factory. The total share count climbs to 150. If you sit on your hands and do not buy any of these new shares, your holding stays stuck at 10 shares.

Your new ownership percentage drops to:

Ownership = 10 / 150 = 6.67%

Look at what just happened. You didn’t sell a single share. You didn’t sign any transfer papers. Yet, your proportional ownership in the company plummeted from 10% to 6.67% simply because the share pool expanded. This is equity dilution.

Why should you care? Because dilution directly chips away at your financial upside. It reduces your voting power at annual meetings, shrinks your slice of future dividend payouts, and dilutes your claim on the company’s net earnings. Preemptive rights exist to ensure this economic erosion never happens behind your back.

How Preemptive Rights Work

When a company that protects preemptive rights wants to raise cash by issuing new equity, it cannot just call up a wealthy outside fund or launch a public campaign right away. It is legally obligated to offer those shares to its loyal, existing shareholders first.

The company will issue “rights” to every shareholder based on their current ownership ratio. Once these rights land in your investment account, you are in the driver’s seat. You generally have three distinct paths to choose from:

Exercise the rights: You pay the designated subscription price and purchase your allotted share of the new stock. By doing this, your exact ownership percentage remains perfectly intact.

Sell the rights: In many public markets, these rights are structured as separate, tradable financial instruments. If you don’t want to invest more cash but want to offset the financial damage of dilution, you can sell your rights on the open market to another investor for hard cash.

Let the rights lapse: You choose to do absolutely nothing. Once the deadline passes, your rights expire, become worthless, and your ownership stake gets diluted.

Simple Numerical Example

Let’s scale this up to a realistic corporate scenario. Suppose a company has 1,00,000 shares outstanding, and you own 10,000 of them.

Your Current Ownership = 10,000 / 1,00,000 = 10%

The board of directors approves a plan to issue 20,000 new shares at ₹50 per share to raise ₹10,00,000 (₹10 lakh) in fresh equity capital. Because you hold preemptive rights, the company must offer you 10% of this new batch before anyone else can touch them.

Your Entitlement = 10% × 20,000 = 2,000 shares

To maintain your 10% grip on the company, you need to write a check for your allocation:

Amount Required = 2,000 shares × ₹50 = ₹1,00,000

If you exercise your rights and invest that ₹1 lakh, let’s look at the post-money math:

Your New Share Balance = 10,000 + 2,000 = 12,000 shares

Total Shares Outstanding = 1,00,000 + 20,000 = 1,20,000 shares

Your New Ownership = 12,000 / 1,20,000 = 10%

Your ownership stake is perfectly preserved, and you successfully avoided any dilution.

What if the Shareholder Does Not Exercise?

What if you don’t have ₹1 lakh sitting around, or you simply don’t want to double down on this particular stock?

If you decide to let your rights lapse, your share count stays exactly where it started at 10,000 shares. However, the company still goes ahead and sells those 20,000 new shares to other investors, pushing the total share pool to 1,20,000.

Your New Diluted Ownership = 10,000 / 1,20,000 = 8.33%

Your structural influence and future earnings claim in the business have dropped from 10% to 8.33%. This drop represents the real economic cost of bypassing your preemptive rights.

The Subscription Price

To encourage investors to participate in a rights issue, companies rarely price these new shares at full market value. Instead, the subscription price is almost always set at a discount to the current market price.

Think about it: if a stock is trading on the stock exchange at ₹80 per share, nobody is going to go through the administrative hassle of a rights issue just to buy it at ₹80. But if the company offers those same shares to existing investors at a subscription price of ₹50, it creates a powerful financial incentive.

This gap between the open-market value and the discounted subscription price gives the right its intrinsic economic value. If you don’t want to buy the shares, you can sell the right itself to someone else, capturing that price difference as a cash consolation prize for your impending dilution.

Theoretical Value of a Right

For finance professionals and students analyzing corporate actions, calculating the exact worth of these entitlements is highly predictable. The theoretical value of a right can be isolated using a standard formula:

Value of One Right = (Market Price − Subscription Price) / (Number of Rights Required to Buy One New Share + 1)

Let’s plug in the numbers from our earlier scenario:

Current Market Price = ₹80

Subscription Price = ₹50

Number of Rights needed to buy 1 new share = 5

Value of One Right = (₹80 − ₹50) / (5 + 1) = ₹30 / 6 = ₹5

In a friction-free market, each individual right has a theoretical value of ₹5. If you decide to pass on the share offering, you can sell your rights on the exchange for roughly ₹5 each, pocketing the cash to offset the economic dilution of your principal investment.

Preemptive Rights in India

In India, preemptive rights are not just an optional luxury buried in a company’s internal bylaws—they are deeply woven into the fabric of corporate law through Section 62 of the Companies Act, 2013.

The law dictates that whenever a company proposes to increase its subscribed capital by issuing fresh shares, it must offer them to existing equity shareholders in proportion to their paid-up capital.

Regulatory guardrails ensure fairness:

The rights offer must remain open for a window of at least 15 days and no more than 30 days.

If a shareholder fails to respond within this legal window, they are deemed to have declined the offer, allowing the company to dispose of the unsubscribed shares as it sees fit.

For publicly listed companies, the Securities and Exchange Board of India (SEBI) adds an extra layer of oversight through its ICDR (Issue of Capital and Disclosure Requirements) Regulations. These rules tightly govern pricing mechanisms, fast-tracked timelines, and mandatory disclosure documents to ensure retail minority investors aren’t left in the dark.

When Can Preemptive Rights Be Bypassed?

Preemptive rights provide strong protection, but they are not absolute. Companies occasionally need to move faster than a 15-to-30-day rights window allows, or they may need to bring a strategic partner on board. There are a few legal backdoors where preemptive rights can be bypassed:

Preferential Allotment: A company can issue shares directly to a select group of investors (like corporate promoters, private equity funds, or institutional partners). However, to do this legally, management must secure a special resolution at a general meeting, meaning the existing shareholders must collectively vote to waive their preemptive rights.

Employee Stock Option Plans (ESOPs): Shares issued to employees as performance incentives or compensation are legally exempt from standard preemptive rights provisions.

Qualified Institutional Placements (QIPs): Listed companies in India frequently use the QIP route to raise large amounts of capital from institutional buyers (like mutual funds or insurance companies) in a matter of days, avoiding the lengthy operational runway of a public rights issue.

Why Preemptive Rights Matter for Corporate Governance

At its core, the presence of preemptive rights is a litmus test for strong corporate governance and minority shareholder protection.

Without these rights, a company’s promoters or majority owners could easily abuse their power. For example, they could authorize a massive issuance of cheap shares to a shell company or a friendly ally, diluting minority investors into irrelevance while tightening their own grip on the boardroom.

Preemptive rights level the playing field. They guarantee that every investor, whether they own 50% or 0.005% of the business, gets the exact same opportunity to preserve their corporate standing.

Preemptive Rights and Private Companies

While preemptive rights are helpful in public markets, they are absolutely vital in the world of startup investing and private companies.

If you own shares in a listed company and get diluted, you can easily tap your brokerage app, sell your position, and walk away. The economic damage stings, but you have an immediate exit.

In a private company, there is no public exchange. If a venture capital firm or an angel investor gets aggressively diluted in a subsequent funding round, they can’t easily sell out. They are stuck holding a smaller, less influential piece of an illiquid asset. This is why you will rarely find a Venture Capital or Private Equity term sheet that does not feature preemptive rights as a non-negotiable clause.

Preemptive Rights vs. Right of First Refusal

Because they sound similar, these two legal concepts are frequently confused, but they govern completely different transactions:

Preemptive Rights trigger when the company creates and issues brand-new shares. It gives you the right to buy from the source before outsiders do.

Right of First Refusal (ROFR) triggers when an existing shareholder wants to pack up and sell their current shares to someone else. It gives you the right to step in and buy those secondary shares before they are sold to an outside party.

| Basis | Preemptive Rights | Right of First Refusal |

| Triggered by | Company issuing brand-new shares | An existing shareholder selling their shares |

| Primary Purpose | Prevent corporate ownership dilution | Control who enters the shareholder base |

| Commonly Found In | Public rights issues, corporate equity rounds | Shareholder agreements, private/closely-held firms |

Exam Perspective

If you are preparing for professional finance designations like the CFA or FRM, keep these fundamental takeaways parked in your notes:

Proportionality is Key: Preemptive rights always operate in proportion to your current holdings to prevent the dilution of voting power and earnings per share (EPS).

The Pricing Discount: Rights issues are almost universally priced below the current market price, giving the underlying right an immediate economic value.

The Valuation Mechanics: Be ready to calculate the theoretical value of a right using the standard corporate actions formula: (Market Price − Subscription Price) / (N + 1).

Regulatory Frameworks: In India, look directly to Section 62 of the Companies Act, 2013, and SEBI’s ICDR guidelines for the rules governing listed entities.

The Governance Shield: Remember that preemptive rights can only be bypassed via corporate mechanisms like preferential allotments, QIPs, or ESOPs with explicit shareholder approval.

Final Thoughts

Preemptive rights are one of those quiet corporate protections that many retail investors completely overlook—right up until the moment they need them most.

Whenever a company decides to raise fresh capital, the conversation shouldn’t just focus on the headline valuation or the total capital raised. The real governance question is: Who gets to participate, and on what terms? Without preemptive rights, minority investors run the risk of watching their corporate influence slowly slip away.

The mathematics behind it are clean, and the underlying logic is indisputable. In a financial landscape where the dilution of minority investors is a historical reality, understanding this right is far more than just a test question—it’s an essential tool for protecting your capital.

Sonnet 4.6 Low