Equity

Quote-Driven Markets: How Dealer Markets Actually Work

Most people learn about financial markets through stock exchanges, a place where buyers and sellers come together, orders get matched, and prices emerge from the interaction of supply and demand. It’s a clean picture. It’s also only half the story.

A large portion of global financial trading doesn’t work this way at all. There’s no central order book, no queue of buyers and sellers waiting to be matched. Instead, there are dealers and financial institutions that stand ready to buy and sell at prices they themselves set. These are quote-driven markets, and once you understand how they work, you start seeing them everywhere: in the bond market, the foreign exchange market, the OTC derivatives market, and several others that collectively dwarf equity exchanges in trading volume.

The Basic Structure

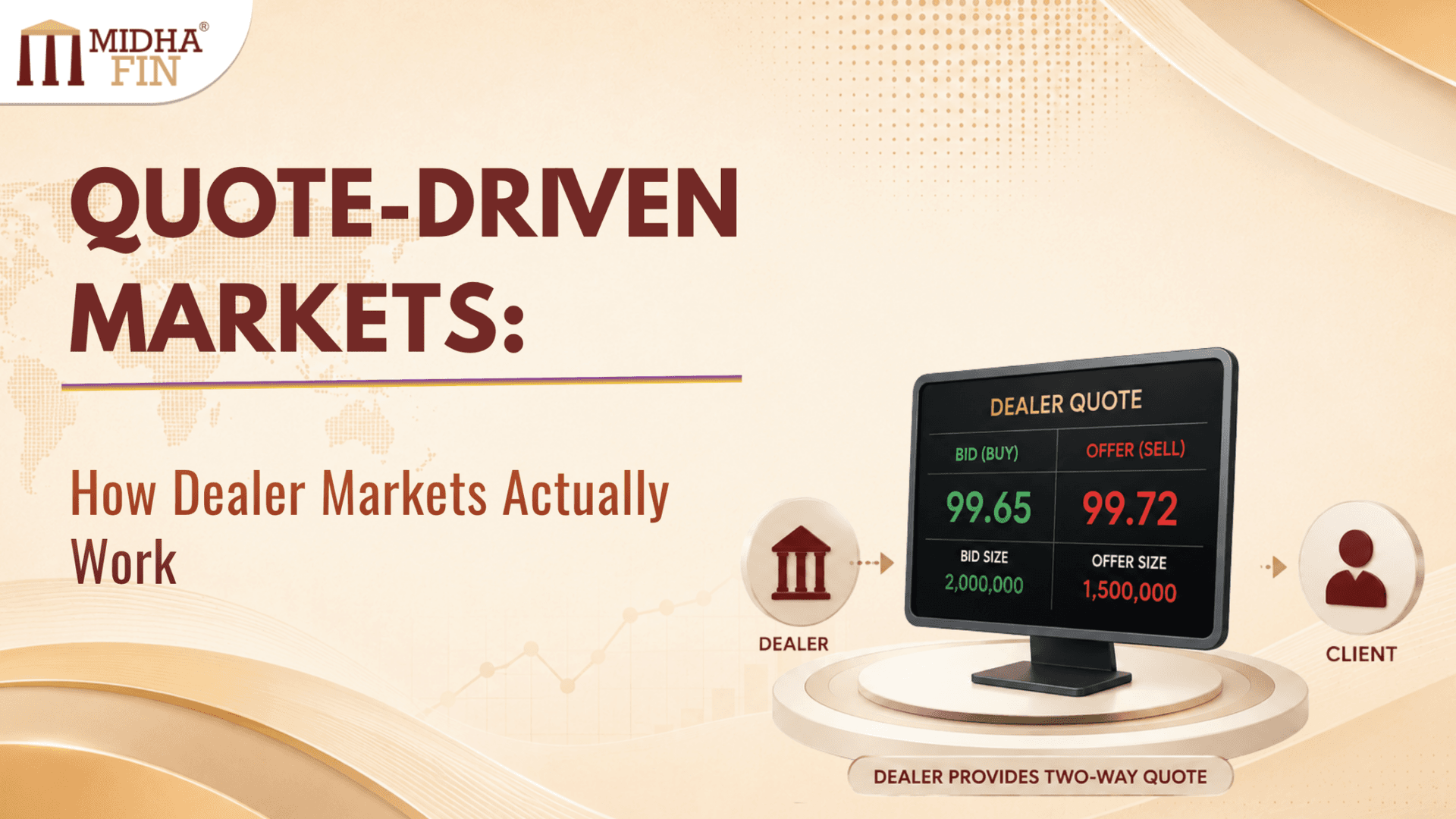

A quote-driven market also called a dealer market or price-driven market is one where designated market makers continuously post bid and ask prices at which they are willing to trade.

The bid is the price at which the dealer will buy from you. The ask (or offer) is the price at which the dealer will sell to you. The difference between the two is the bid-ask spread, and it is the dealer’s primary source of compensation for providing liquidity.

If you want to buy, you pay the ask. If you want to sell, you receive the bid. The dealer sits in the middle, buying at the lower price and selling at the higher price, collecting the spread on each transaction.

This is fundamentally different from an order-driven market, a stock exchange like the NSE or BSE where buyers and sellers interact directly through a central limit order book. In an order-driven market, prices emerge from the matching of competing orders. In a quote-driven market, prices are set by dealers who are obligated or at least expected to make a market continuously.

Who Are the Dealers and What Are They Actually Doing?

The dealers in quote-driven markets are typically large financial institutions, investment banks, commercial banks, and specialist trading firms. In the government bond market, they’re called primary dealers. In foreign exchange, they’re the major global banks. In OTC derivatives, they’re the same institutions running large trading books.

What a dealer is doing at any given moment is more complex than it looks from the outside. When a dealer quotes a bid and an ask, they’re not simply acting as a matchmaker. They’re taking on inventory risk buying securities they might not immediately be able to sell, or selling securities they might have to buy back later at a higher price.

Think about it from the dealer’s perspective. A large institutional investor calls and wants to sell ₹500 crore of a particular government bond. The dealer buys it immediately, at the quoted bid price, without knowing who the next buyer will be or when they’ll appear. The dealer now holds ₹500 crore of that bond on their balance sheet. If yields rise before they can offload it, they take a loss. That inventory risk is real, and the bid-ask spread is partly compensation for bearing it.

This is why understanding dealer markets requires thinking about dealers not as passive intermediaries but as active risk-takers who are continuously managing a book of positions, hedging exposures, and trying to earn the spread while controlling their inventory risk.

The Bid-Ask Spread: More Than Just a Transaction Cost

The bid-ask spread is the most visible feature of a quote-driven market, and it’s worth understanding what actually drives it because it’s not arbitrary.

Inventory risk is the biggest factor. When a dealer takes on a large position, they’re exposed to adverse price movements until they can offload it. In volatile markets, that exposure is larger, and dealers widen spreads to compensate. This is why spreads tend to blow out during periods of market stress dealers are still providing liquidity, but they’re charging more for it.

Adverse selection risk is subtler but equally important. Not everyone who trades with a dealer has the same information. Some traders are informed they know something about the security’s true value that the dealer doesn’t. When an informed trader sells to the dealer, the dealer is likely buying at a price that’s too high. When the dealer doesn’t know whether the counterparty is informed or not, they widen the spread to protect against the possibility of trading against better-informed participants. This is the classic adverse selection problem in market microstructure theory.

Order processing costs back-office operations, technology, compliance are a smaller but real component of the spread.

Competition matters significantly. When multiple dealers are quoting on the same security, they compete on spread width to attract order flow. Tighter competition means tighter spreads. In markets with few active dealers of illiquid bonds, exotic derivatives spreads can be wide simply because there’s limited competition forcing them down.

Where Quote-Driven Markets Dominate

Government and Corporate Bond Markets

The fixed income market is the largest quote-driven market in the world. Most bonds, government securities, corporate bonds, municipal bonds trade over the counter through dealers rather than on centralised exchanges.

In India, the government securities market operates through a network of primary dealers institutions like SBI DFHI, ICICI Securities Primary Dealership, and others who are obligated to participate in government auctions and make secondary markets in G-Secs. When a bank or institution wants to buy or sell a government bond, they typically call a primary dealer for a quote rather than routing through an exchange.

The reason bonds trade this way rather than on exchanges comes down to the sheer variety of instruments. Indian equity markets have a few thousand listed stocks. The bond market has tens of thousands of individual securities of different maturities, different coupon rates, different issuers most of which trade infrequently. A centralised order book for each would be mostly empty. Dealers solve this problem by aggregating liquidity across counterparties and providing quotes on demand.

Foreign Exchange

The global forex market averaging over $7 trillion in daily turnover is almost entirely quote-driven. When a company wants to convert dollars to rupees, or an investor wants to buy euros, they get a quote from a bank. The bank quotes a bid and an ask, the transaction happens bilaterally, and the bank manages the resulting position in the interbank market.

The interbank forex market is itself a dealer market large banks quote prices to each other and trade bilaterally. Electronic platforms like Reuters Matching and EBS have brought more transparency and tighter spreads to this market, but the underlying structure remains quote-driven.

OTC Derivatives

Interest rate swaps, credit default swaps, currency forwards, and most structured products trade over the counter through dealers. The dealer takes the other side of the trade, quotes a price that includes their compensation, and manages the resulting risk through hedging.

Post-2008, regulatory reforms pushed many standardised OTC derivatives toward centralised clearing which reduces counterparty risk but the price discovery process and initial trading remain largely dealer-driven.

Quote-Driven vs Order-Driven: The Key Differences

Understanding both systems and what distinguishes them is central to the CFA curriculum’s treatment of market structure.

In an order-driven market, price discovery happens through the interaction of buyers and sellers submitting competing orders. The market is transparent; you can see the order book, know what prices are available, and observe trading interest at different levels. Execution happens automatically when orders match. There’s no designated intermediary bearing inventory risk; if no one wants to buy what you’re selling at your price, the order sits in the queue.

In a quote-driven market, price discovery happens through dealer quotes. Transparency is lower when you see the dealer’s quote but not the full picture of supply and demand behind it. Execution is immediate; the dealer is obligated to trade at their quoted price but the price you get depends on the dealer’s assessment of their inventory, their view of the market, and what they think the security is worth.

The tradeoff is essentially immediacy versus transparency. Quote-driven markets provide guaranteed immediacy a dealer will trade with you right now at a stated price. Order-driven markets provide transparency; you can see exactly where the market is but execution depends on finding a matching counterparty.

For large trades in illiquid instruments, quote-driven markets are often more practical. Breaking a large bond trade into small pieces on an exchange-style system can be slow, signal your intentions to the market, and result in worse average execution than simply calling a dealer for a firm price on the whole block.

Transparency and Its Limitations

One persistent criticism of quote-driven markets is the relative lack of transparency compared to exchange-traded markets.

In an equity market, every trade is reported, prices are publicly disseminated in real time, and the order book is visible. In an OTC bond market, historically, prices were known only to the parties involved. A dealer could quote different prices to different clients for the same security, and clients had limited ability to know whether they were getting a fair price.

Regulatory efforts have pushed toward more transparency in OTC markets. In the US, TRACE (Trade Reporting and Compliance Engine) now requires post-trade reporting for most bond transactions, making prices visible after the fact. SEBI has been pushing for greater transparency in India’s corporate bond market for similar reasons improving price discovery and reducing information asymmetry between dealers and investors.

But pre-trade transparency knowing what prices are available before you trade remains limited in most OTC markets compared to exchanges. This is a structural feature, not just a regulatory gap, because dealers’ ability to manage inventory risk depends partly on not telegraphing their positions to the market before they’ve had a chance to hedge.

Market Making and Liquidity Provision

In many quote-driven markets, certain dealers have formal obligations to make markets to post continuous bid and ask prices regardless of market conditions. These obligations are typically tied to privileges, such as access to central bank facilities, preferred status in government bond auctions, or fee rebates.

Primary dealers in India’s G-Sec market, for example, have underwriting obligations at government bond auctions in exchange for their status. The implicit deal is: you support government borrowing when needed, and in return you get access and privileges that make market-making commercially viable.

During market stress when volatility spikes and inventory risk rises sharply this formal market-making obligation becomes genuinely costly for dealers. The 2008 financial crisis illustrated what happens when dealer balance sheets become constrained and dealers pull back from market-making: bid-ask spreads widen dramatically, markets become illiquid, and price discovery breaks down. The capacity of the dealer system to absorb risk is a binding constraint on market liquidity that doesn’t exist in the same form in pure order-driven markets.

Hybrid Markets

Most modern financial markets are actually hybrids combining elements of both quote-driven and order-driven systems.

The NSE and BSE are primarily order-driven, but they have designated market makers for less liquid stocks and ETFs dealers who post continuous quotes to ensure that small investors can always find a price. This injects quote-driven liquidity into what is otherwise an order-driven system.

Conversely, some OTC markets have developed electronic platforms that aggregate dealer quotes and allow investors to compare prices across multiple dealers before trading moving toward the transparency of order-driven markets while retaining the dealer structure underneath.

SEBI’s push to develop India’s corporate bond market has involved encouraging electronic platforms that display multiple dealer quotes, precisely to address the transparency limitations of a purely OTC, bilateral market.

Key Takeaways for the Exam

A quote-driven market is one where dealers post continuous bid and ask prices and stand ready to trade at those prices contrasting with order-driven markets where prices emerge from matching buyer and seller orders. The bid-ask spread is the dealer’s primary compensation and reflects inventory risk, adverse selection risk, order processing costs, and competitive dynamics. Dealers are active risk-takers who manage inventory positions, not passive intermediaries. Quote-driven markets dominate in fixed income, foreign exchange, and OTC derivatives markets where instrument variety or trade size makes centralised order books impractical. The key tradeoff versus order-driven markets is immediacy versus transparency dealer markets offer guaranteed execution but lower pre-trade price visibility. Market-making obligations in formal dealer systems like primary dealers in government bond markets tie liquidity provision to specific privileges and responsibilities. Regulatory trends globally have pushed for greater post-trade transparency in OTC markets without fundamentally changing the dealer structure.

The bond market, the forex market, the derivatives market these are the markets where most of the world’s capital actually moves, and they all run on the dealer model. Understanding quote-driven markets isn’t just an exam topic. It’s the foundation for understanding how liquidity is actually created and destroyed in financial systems, why spreads widen in stress, and why the health of dealer balance sheets matters so much to the functioning of markets as a whole.Most people learn about financial markets through stock exchanges, a place where buyers and sellers come together, orders get matched, and prices emerge from the interaction of supply and demand. It’s a clean picture. It’s also only half the story.

A large portion of global financial trading doesn’t work this way at all. There’s no central order book, no queue of buyers and sellers waiting to be matched. Instead, there are dealers and financial institutions that stand ready to buy and sell at prices they themselves set. These are quote-driven markets, and once you understand how they work, you start seeing them everywhere: in the bond market, the foreign exchange market, the OTC derivatives market, and several others that collectively dwarf equity exchanges in trading volume.

The Basic Structure

A quote-driven market also called a dealer market or price-driven market is one where designated market makers continuously post bid and ask prices at which they are willing to trade.

The bid is the price at which the dealer will buy from you. The ask (or offer) is the price at which the dealer will sell to you. The difference between the two is the bid-ask spread, and it is the dealer’s primary source of compensation for providing liquidity.

If you want to buy, you pay the ask. If you want to sell, you receive the bid. The dealer sits in the middle, buying at the lower price and selling at the higher price, collecting the spread on each transaction.

This is fundamentally different from an order-driven market, a stock exchange like the NSE or BSE where buyers and sellers interact directly through a central limit order book. In an order-driven market, prices emerge from the matching of competing orders. In a quote-driven market, prices are set by dealers who are obligated or at least expected to make a market continuously.

Who Are the Dealers and What Are They Actually Doing?

The dealers in quote-driven markets are typically large financial institutions, investment banks, commercial banks, and specialist trading firms. In the government bond market, they’re called primary dealers. In foreign exchange, they’re the major global banks. In OTC derivatives, they’re the same institutions running large trading books.

What a dealer is doing at any given moment is more complex than it looks from the outside. When a dealer quotes a bid and an ask, they’re not simply acting as a matchmaker. They’re taking on inventory risk buying securities they might not immediately be able to sell, or selling securities they might have to buy back later at a higher price.

Think about it from the dealer’s perspective. A large institutional investor calls and wants to sell ₹500 crore of a particular government bond. The dealer buys it immediately, at the quoted bid price, without knowing who the next buyer will be or when they’ll appear. The dealer now holds ₹500 crore of that bond on their balance sheet. If yields rise before they can offload it, they take a loss. That inventory risk is real, and the bid-ask spread is partly compensation for bearing it.

This is why understanding dealer markets requires thinking about dealers not as passive intermediaries but as active risk-takers who are continuously managing a book of positions, hedging exposures, and trying to earn the spread while controlling their inventory risk.

The Bid-Ask Spread: More Than Just a Transaction Cost

The bid-ask spread is the most visible feature of a quote-driven market, and it’s worth understanding what actually drives it because it’s not arbitrary.

Inventory risk is the biggest factor. When a dealer takes on a large position, they’re exposed to adverse price movements until they can offload it. In volatile markets, that exposure is larger, and dealers widen spreads to compensate. This is why spreads tend to blow out during periods of market stress dealers are still providing liquidity, but they’re charging more for it.

Adverse selection risk is subtler but equally important. Not everyone who trades with a dealer has the same information. Some traders are informed they know something about the security’s true value that the dealer doesn’t. When an informed trader sells to the dealer, the dealer is likely buying at a price that’s too high. When the dealer doesn’t know whether the counterparty is informed or not, they widen the spread to protect against the possibility of trading against better-informed participants. This is the classic adverse selection problem in market microstructure theory.

Order processing costs back-office operations, technology, compliance are a smaller but real component of the spread.

Competition matters significantly. When multiple dealers are quoting on the same security, they compete on spread width to attract order flow. Tighter competition means tighter spreads. In markets with few active dealers of illiquid bonds, exotic derivatives spreads can be wide simply because there’s limited competition forcing them down.

Where Quote-Driven Markets Dominate

Government and Corporate Bond Markets

The fixed income market is the largest quote-driven market in the world. Most bonds, government securities, corporate bonds, municipal bonds trade over the counter through dealers rather than on centralised exchanges.

In India, the government securities market operates through a network of primary dealers institutions like SBI DFHI, ICICI Securities Primary Dealership, and others who are obligated to participate in government auctions and make secondary markets in G-Secs. When a bank or institution wants to buy or sell a government bond, they typically call a primary dealer for a quote rather than routing through an exchange.

The reason bonds trade this way rather than on exchanges comes down to the sheer variety of instruments. Indian equity markets have a few thousand listed stocks. The bond market has tens of thousands of individual securities of different maturities, different coupon rates, different issuers most of which trade infrequently. A centralised order book for each would be mostly empty. Dealers solve this problem by aggregating liquidity across counterparties and providing quotes on demand.

Foreign Exchange

The global forex market averaging over $7 trillion in daily turnover is almost entirely quote-driven. When a company wants to convert dollars to rupees, or an investor wants to buy euros, they get a quote from a bank. The bank quotes a bid and an ask, the transaction happens bilaterally, and the bank manages the resulting position in the interbank market.

The interbank forex market is itself a dealer market large banks quote prices to each other and trade bilaterally. Electronic platforms like Reuters Matching and EBS have brought more transparency and tighter spreads to this market, but the underlying structure remains quote-driven.

OTC Derivatives

Interest rate swaps, credit default swaps, currency forwards, and most structured products trade over the counter through dealers. The dealer takes the other side of the trade, quotes a price that includes their compensation, and manages the resulting risk through hedging.

Post-2008, regulatory reforms pushed many standardised OTC derivatives toward centralised clearing which reduces counterparty risk but the price discovery process and initial trading remain largely dealer-driven.

Quote-Driven vs Order-Driven: The Key Differences

Understanding both systems and what distinguishes them is central to the CFA curriculum’s treatment of market structure.

In an order-driven market, price discovery happens through the interaction of buyers and sellers submitting competing orders. The market is transparent; you can see the order book, know what prices are available, and observe trading interest at different levels. Execution happens automatically when orders match. There’s no designated intermediary bearing inventory risk; if no one wants to buy what you’re selling at your price, the order sits in the queue.

In a quote-driven market, price discovery happens through dealer quotes. Transparency is lower when you see the dealer’s quote but not the full picture of supply and demand behind it. Execution is immediate; the dealer is obligated to trade at their quoted price but the price you get depends on the dealer’s assessment of their inventory, their view of the market, and what they think the security is worth.

The tradeoff is essentially immediacy versus transparency. Quote-driven markets provide guaranteed immediacy a dealer will trade with you right now at a stated price. Order-driven markets provide transparency; you can see exactly where the market is but execution depends on finding a matching counterparty.

For large trades in illiquid instruments, quote-driven markets are often more practical. Breaking a large bond trade into small pieces on an exchange-style system can be slow, signal your intentions to the market, and result in worse average execution than simply calling a dealer for a firm price on the whole block.

Transparency and Its Limitations

One persistent criticism of quote-driven markets is the relative lack of transparency compared to exchange-traded markets.

In an equity market, every trade is reported, prices are publicly disseminated in real time, and the order book is visible. In an OTC bond market, historically, prices were known only to the parties involved. A dealer could quote different prices to different clients for the same security, and clients had limited ability to know whether they were getting a fair price.

Regulatory efforts have pushed toward more transparency in OTC markets. In the US, TRACE (Trade Reporting and Compliance Engine) now requires post-trade reporting for most bond transactions, making prices visible after the fact. SEBI has been pushing for greater transparency in India’s corporate bond market for similar reasons improving price discovery and reducing information asymmetry between dealers and investors.

But pre-trade transparency knowing what prices are available before you trade remains limited in most OTC markets compared to exchanges. This is a structural feature, not just a regulatory gap, because dealers’ ability to manage inventory risk depends partly on not telegraphing their positions to the market before they’ve had a chance to hedge.

Market Making and Liquidity Provision

In many quote-driven markets, certain dealers have formal obligations to make markets to post continuous bid and ask prices regardless of market conditions. These obligations are typically tied to privileges, such as access to central bank facilities, preferred status in government bond auctions, or fee rebates.

Primary dealers in India’s G-Sec market, for example, have underwriting obligations at government bond auctions in exchange for their status. The implicit deal is: you support government borrowing when needed, and in return you get access and privileges that make market-making commercially viable.

During market stress when volatility spikes and inventory risk rises sharply this formal market-making obligation becomes genuinely costly for dealers. The 2008 financial crisis illustrated what happens when dealer balance sheets become constrained and dealers pull back from market-making: bid-ask spreads widen dramatically, markets become illiquid, and price discovery breaks down. The capacity of the dealer system to absorb risk is a binding constraint on market liquidity that doesn’t exist in the same form in pure order-driven markets.

Hybrid Markets

Most modern financial markets are actually hybrids combining elements of both quote-driven and order-driven systems.

The NSE and BSE are primarily order-driven, but they have designated market makers for less liquid stocks and ETFs dealers who post continuous quotes to ensure that small investors can always find a price. This injects quote-driven liquidity into what is otherwise an order-driven system.

Conversely, some OTC markets have developed electronic platforms that aggregate dealer quotes and allow investors to compare prices across multiple dealers before trading moving toward the transparency of order-driven markets while retaining the dealer structure underneath.

SEBI’s push to develop India’s corporate bond market has involved encouraging electronic platforms that display multiple dealer quotes, precisely to address the transparency limitations of a purely OTC, bilateral market.

Key Takeaways for the Exam

A quote-driven market is one where dealers post continuous bid and ask prices and stand ready to trade at those prices contrasting with order-driven markets where prices emerge from matching buyer and seller orders. The bid-ask spread is the dealer’s primary compensation and reflects inventory risk, adverse selection risk, order processing costs, and competitive dynamics. Dealers are active risk-takers who manage inventory positions, not passive intermediaries. Quote-driven markets dominate in fixed income, foreign exchange, and OTC derivatives markets where instrument variety or trade size makes centralised order books impractical. The key tradeoff versus order-driven markets is immediacy versus transparency dealer markets offer guaranteed execution but lower pre-trade price visibility. Market-making obligations in formal dealer systems like primary dealers in government bond markets tie liquidity provision to specific privileges and responsibilities. Regulatory trends globally have pushed for greater post-trade transparency in OTC markets without fundamentally changing the dealer structure.

The bond market, the forex market, the derivatives market these are the markets where most of the world’s capital actually moves, and they all run on the dealer model. Understanding quote-driven markets isn’t just an exam topic. It’s the foundation for understanding how liquidity is actually created and destroyed in financial systems, why spreads widen in stress, and why the health of dealer balance sheets matters so much to the functioning of markets as a whole.