Quants

Indicator Variables in Linear Regression: Making Sense of Categories in a Numerical World

Regression is built on numbers. You feed it data, it finds relationships, and it gives you coefficients you can interpret. Simple enough — until your data includes something like industry type, gender, a recession period, or whether a company paid a dividend that year. These aren’t numbers. They’re categories. And you can’t just throw categories into a regression equation and expect it to behave.

This is where indicator variables come in. They’re one of the more elegant solutions in applied statistics — a way to bring qualitative information into a quantitative framework without distorting the analysis.

What Is an Indicator Variable?

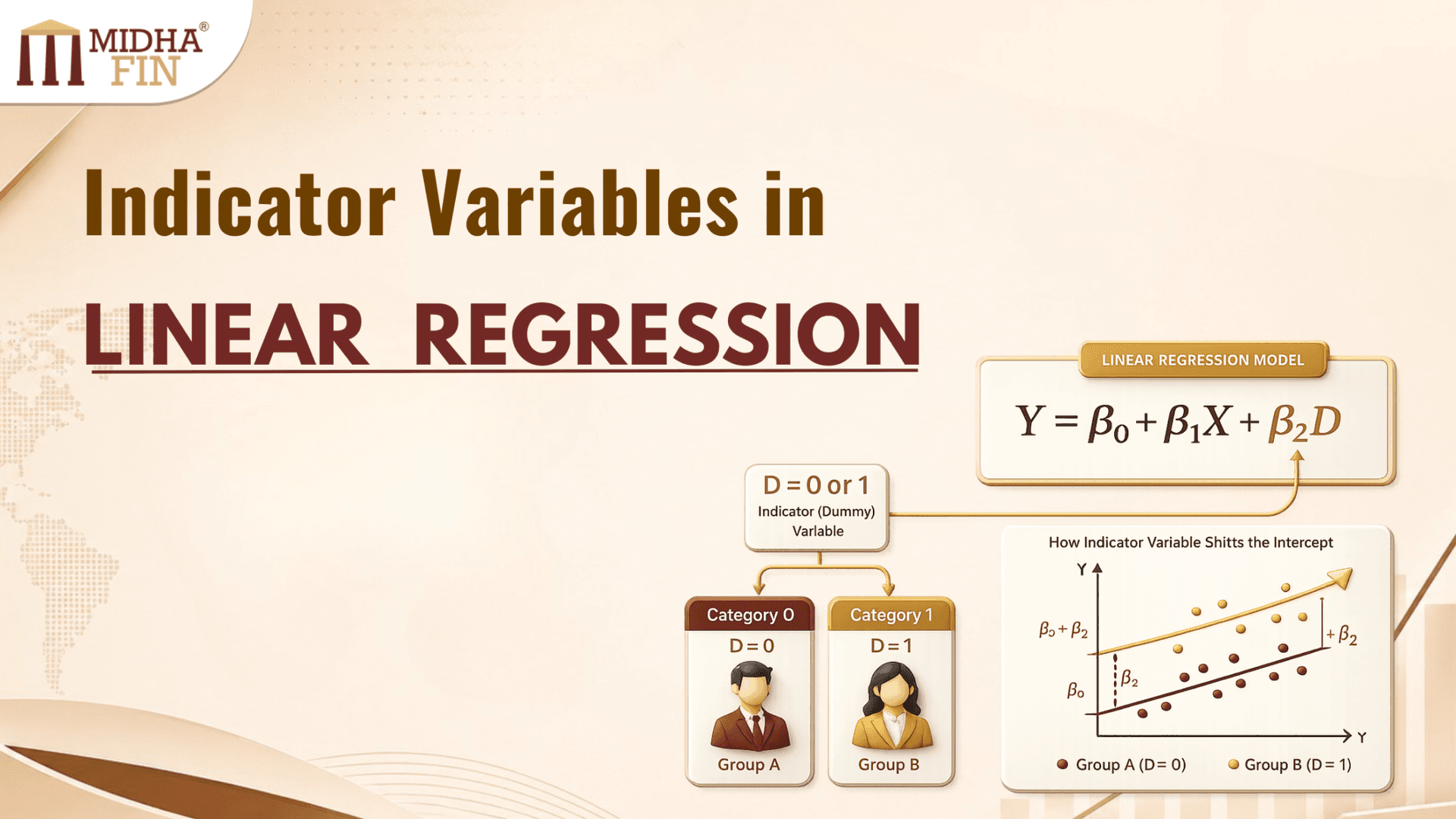

An indicator variable — also called a dummy variable — is a binary variable that takes only two values: 0 or 1.

The 1 indicates the presence of some characteristic. The 0 indicates its absence.

That’s it. The entire idea rests on this simple encoding.

For example:

- Did the quarter fall during a recession? 1 = yes, 0 = no

- Is the company in the financial sector? 1 = yes, 0 = no

- Did the firm pay a dividend this year? 1 = yes, 0 = no

- Is the observation from the post-reform period? 1 = yes, 0 = no

By converting a qualitative distinction into a 0/1 variable, you give the regression model something it can work with mathematically — while preserving the real-world meaning of the distinction.

How It Works in a Regression Model

Consider a simple regression where you’re trying to explain a company’s return on equity (ROE) using its revenue growth and whether it operates in a regulated industry.

The model might look like this:

ROE = β₀ + β₁(Revenue Growth) + β₂(Regulated) + ε

Where “Regulated” is an indicator variable — 1 if the company is in a regulated industry, 0 if it isn’t.

Now think about what β₂ actually represents.

When Regulated = 0 (unregulated company):

ROE = β₀ + β₁(Revenue Growth)

When Regulated = 1 (regulated company):

ROE = (β₀ + β₂) + β₁(Revenue Growth)

The indicator variable shifts the intercept of the regression line. For regulated companies, the baseline ROE is different — higher or lower by β₂ — while the relationship between revenue growth and ROE (captured by β₁) stays the same.

This is the key intuition: an indicator variable changes the intercept, not the slope. It shifts the entire regression line up or down for observations in that category.

If β₂ turns out to be −3.5, it means regulated companies have, on average, an ROE that is 3.5 percentage points lower than unregulated companies, holding revenue growth constant.

Interpreting the Coefficient

The coefficient on an indicator variable is always interpreted as the difference in the dependent variable between the group coded as 1 and the group coded as 0, holding all other variables constant.

This “holding other variables constant” part matters. The indicator variable isn’t just comparing raw averages between two groups — it’s doing so after controlling for everything else in the model. That’s what makes regression with indicator variables more useful than a simple group comparison.

A quick example with Indian market context:

Suppose you’re modelling stock returns and you include an indicator variable for whether the stock is a PSU (public sector undertaking). If the coefficient on the PSU dummy comes out as −4.2%, it suggests that PSU stocks, on average, generate returns 4.2 percentage points lower than comparable private sector stocks — after controlling for size, leverage, and other factors in the model.

That’s a much more meaningful statement than simply saying “PSUs have lower average returns,” because it isolates the effect of ownership type from other differences between the groups.

Handling More Than Two Categories

This is where people often make a critical mistake.

Suppose you want to include a variable for industry sector — and you have four sectors: manufacturing, financial services, technology, and healthcare. You might be tempted to create one variable and assign values 1, 2, 3, and 4.

Don’t do this.

Assigning numerical codes to categories implies an ordering and equal spacing that doesn’t exist. It would tell the model that technology (3) is somehow halfway between financial services (2) and healthcare (4), which is meaningless.

The correct approach is to create multiple indicator variables — one for each category, minus one.

So for four sectors, you create three indicator variables:

- D₁ = 1 if Financial Services, 0 otherwise

- D₂ = 1 if Technology, 0 otherwise

- D₃ = 1 if Healthcare, 0 otherwise

Manufacturing is left out. It becomes the reference category — the baseline against which all others are compared.

The regression model then looks like:

Return = β₀ + β₁(D₁) + β₂(D₂) + β₃(D₃) + other variables + ε

Here, β₀ captures the baseline return for manufacturing companies. β₁ tells you how much higher or lower financial services companies’ returns are compared to manufacturing, and so on.

The Dummy Variable Trap

If you have four categories and create four indicator variables — one for each — you fall into what’s called the dummy variable trap.

The four dummy variables will always sum to 1 for every observation (since every company belongs to exactly one sector). This creates perfect multicollinearity — one variable is a perfect linear combination of the others. The regression cannot be estimated.

The rule is simple: if a qualitative variable has k categories, include k−1 indicator variables. Always leave one category out as the reference group.

The choice of reference category doesn’t affect the substance of the results — it only changes what the comparisons are made against. Choose a reference category that makes the comparisons intuitive and meaningful.

Indicator Variables for Time and Structural Breaks

One particularly useful application in financial analysis is using indicator variables to capture structural breaks — points in time where the relationship in the data fundamentally changed.

Suppose you’re modelling Indian corporate profit margins over a long time series that spans before and after GST implementation. The tax regime changed structurally in 2017, and margins may have shifted in ways unrelated to the usual business cycle factors.

You could include an indicator variable:

Post_GST = 1 for observations from July 2017 onwards, 0 before

This allows the model to capture the shift in baseline margins after GST, without forcing you to run two completely separate regressions.

Similarly, analysts modelling returns during COVID-affected periods often include a pandemic indicator to absorb the unusual observations from 2020 and early 2021, rather than letting those extreme data points distort the estimated relationships for normal periods.

Interaction Terms: When the Slope Also Changes

So far, indicator variables have only shifted the intercept. But sometimes, the relationship between two variables is fundamentally different across categories — not just the baseline, but the slope itself.

For example, maybe revenue growth predicts ROE differently for regulated versus unregulated companies. Not just a different starting point, but a different sensitivity.

To capture this, you create an interaction term — the indicator variable multiplied by the continuous variable:

ROE = β₀ + β₁(Revenue Growth) + β₂(Regulated) + β₃(Regulated × Revenue Growth) + ε

Now:

For unregulated companies (Regulated = 0):

ROE = β₀ + β₁(Revenue Growth)

For regulated companies (Regulated = 1):

ROE = (β₀ + β₂) + (β₁ + β₃)(Revenue Growth)

Both the intercept and the slope are different for regulated companies. β₃ tells you by how much the slope changes.

Interaction terms are powerful but require careful interpretation. Adding them without economic justification can lead to overfitting and results that are hard to explain.

Indicator Variables in the CFA Curriculum

In the CFA curriculum, indicator variables appear primarily within quantitative methods — specifically in multiple regression analysis. Key exam points include:

Interpretation: The coefficient on a dummy variable represents the average difference in the dependent variable between the coded group and the reference group, holding other variables constant.

Dummy variable trap: With k categories, include only k−1 dummies. Including all k creates perfect multicollinearity and the model cannot be solved.

Reference category: The omitted category is the baseline. All coefficients on indicator variables are interpreted relative to this baseline.

Seasonal dummies: A common application in time series — using quarterly dummies (three variables for four quarters) to capture seasonal patterns in data like retail sales, earnings, or commodity prices.

Structural break testing: Indicator variables are used to test whether a relationship changed at a specific point in time — relevant in macroeconomic and financial time series analysis.

Interaction terms: When the effect of a continuous variable differs across categories, interaction terms between the dummy and the continuous variable capture this.

A Worked Example

You are modelling quarterly earnings growth for Indian listed companies using the following variables:

- GDP growth (continuous)

- Interest rate level (continuous)

- Q4 indicator (1 if the observation is Q4, 0 otherwise) — capturing the typical year-end earnings boost

- NBFC indicator (1 if the company is an NBFC, 0 otherwise)

Estimated model:

Earnings Growth = 1.2 + 0.8(GDP Growth) − 0.5(Interest Rate) + 2.1(Q4) − 1.8(NBFC)

Reading the coefficients:

- Every 1% increase in GDP growth is associated with 0.8% higher earnings growth, all else equal

- Every 1% rise in interest rates is associated with 0.5% lower earnings growth

- Q4 quarters show earnings growth that is, on average, 2.1% higher than other quarters — capturing seasonality

- NBFCs show earnings growth that is, on average, 1.8% lower than non-NBFCs — after controlling for GDP growth and interest rates

The indicator variables here are doing exactly what they’re designed to do — isolating the effect of a categorical distinction while the continuous variables do their usual work.

Key Takeaways for the Exam

An indicator (dummy) variable takes values of 0 or 1 to represent the absence or presence of a categorical characteristic. Its coefficient measures the average difference in the dependent variable between the two groups, holding other variables constant. For a variable with k categories, use k−1 dummies — always omit one as the reference category. Including all k dummies causes perfect multicollinearity — the dummy variable trap. Interaction terms between a dummy and a continuous variable allow the slope to differ across categories, not just the intercept. Common applications include capturing seasonality, structural breaks, sector effects, and policy changes in financial data.